Nepal Budget

Fiscal Year 2079/80

DOWNLOAD Budget Speech For Fiscal Year 2079/80

- Budget At A Glance

- Prime Minister : Sher Bahadur Deuba

- Finance Minister : Janardan Sharma

- Total Budget : Rs. 17.93 Kharba

DOWNLOAD Budget Speech in pdf Nepali For Fiscal Year 2079/80 2022/23

Nepal Budget 2079/080 2022/023

The nepal budget 2079 / 80 is revealed by the ministry of finance nepal (mof - ministry of finance) nepal budget, budget 2079 80, budget of nepal 2079 80, budget of nepal (bajet 2079 80 nepali - नेपालको बजेट ). By finance minister of nepal - Janardan Sharma on 29-MAY-2022Budget hightlight fiscal year 2079/80 2022/23

- Government Employee salary increased by 15%.

- Rs 6 Arba has been allocated for health in the states and Rs 27 Arba at the local level.

- The government has introduced Kisan Pension Scheme. The government will deposit 10 percent of the amount deposited by the farmers in this scheme.

- Rs 500,000 minimum income tax slab for unmarried people & Rs 600,000 minimum income tax slab for married people.

- LPG subsidy will be removed, the price of cooking gas will increase.

- Announcement to start technical education in 12 hundred schools across the country.

- IPO of Nepal Electricity Authority granted at a premium price. To invest the collected amount in the project containing the reservoir.

- People who consume less than 20 Units of electricity should not pay the price of electricity.

- Gautam Buddha International Cricket Stadium to be taken over by the government.

- Kirtipur stadium to be upgraded to host night time events.

- 10% share quota for IPOs to be allocated for the Nepali investors living abroad.

- Rs 10 crores has been allocated for the procurement of internet and digital boards in 20 schools in all provinces.

- Budget Speech 2079/80

Fiscal Year 2078/79

DOWNLOAD Budget Speech For Fiscal Year 2078/79

- Budget At A Glance

- Prime Minister : KP Sharma Oli

- Finance Minister : Bishnu Prasad Paudel

- Total Budget : Rs. 1,647.57 Billion

DOWNLOAD Budget Speech in pdf Nepali For Fiscal Year 2078/79 2021/22

Nepal Budget 2078/079 2021/022

The nepal budget 2078 79 is revealed by the ministry of finance nepal (mof - ministry of finance) nepal budget, budget 2077 78, budget of nepal 2077 78, budget of nepal (bajet 2078 79 nepali - नेपालको बजेट ). By finance minister of nepal - Bishnu Prasad Paudel on 29-MAY-2021Budget hightlight fiscal year 2078/79 2021/22

- Government Employee salary increased by Rs. 2,000/- for all level.

- "Made in Nepal & make in Nepal" programs will be launched to promote local product.

- The budget for Railway 10 Arba 3 Karod

- The budget for Yuwa tatha khelkud sector is 2 Arba 74 karod

- The budget for education sector is 1 kharba 80 Arba 4 Karod

- The budget for Health sector is 1 kharba 22 Arba

- School employee and ECD teachers (Bidhyalaya karmachari ra Bal bikas sikshak) salary increased to Rs. 15,000/-

- Government Employee will have 10 Days paid leave.

- Student above 16 years age will receive free Mobile SIM

- Student above 16 years may benifited loan for Laptop Purchase up to Rs. 80,000/- by 1% interest rate.

- Briddha Bhatta increase to Rs. 4,000/-

- Mahila Swasthya Swayam Sebika transportation allowance increased to Rs, 12,000/-.

- Student will receive 25 Lakh loan by collatoring their bachelor certificate in 5% interest rate.

- Budget for Aggriculture 45 Arba 9 Karod

- Budget for Covid-19 CORONA prevention & Cure 37 Arba 57 Karod

- Poverty Alleviation Fund - PAF (Garibi Niwaran kosh) dissolved.

- 500 Charging station will setup for electric vehicles

- Budget for Covid vaccination 26 Arba 75 karod

- Food allowance for Defence sector (Army, police, APF) increased by 15%

- Samsad Bikash Kosh Kharej

- No income tax for income from Mutual Fund

- Budget Speech 2078/79

Fiscal Year 2077/78

DOWNLOADBudget Speech For Fiscal Year 2077/78

- Budget At A Glance

- Prime Minister : KP Sharma Oli

- Finance Minister : Dr. Yuvaraj Khatiwada

- Total Budget : NPR 1.47 trillion

Fiscal Year 2076/77

DOWNLOADBudget Speech For Fiscal Year 2076/77

- Budget At A Glance

- Prime Minister : KP Sharma Oli

- Finance Minister : Dr. Yuvaraj Khatiwada

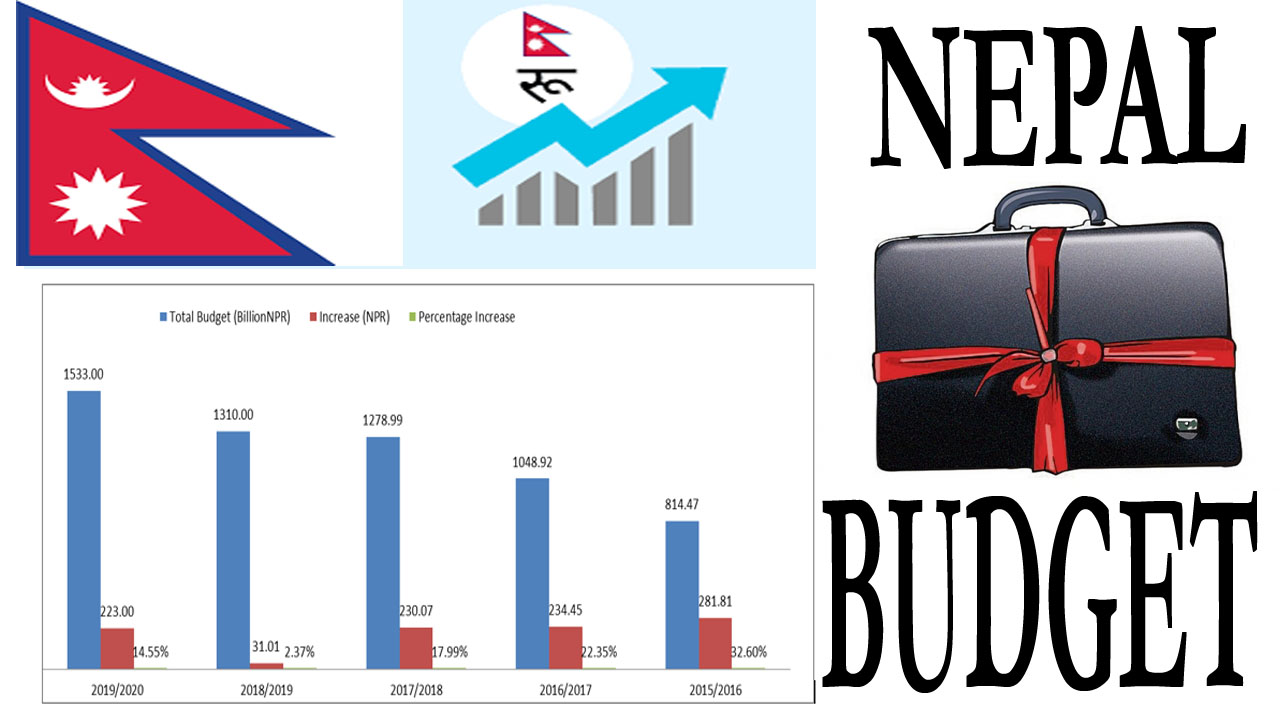

- Total Budget : NPR 1.53 trillion

Fiscal Year 2075/76

DOWNLOADBudget Speech For Fiscal Year 2075/76

- Budget At A Glance

- Prime Minister : KP Sharma Oli

- Finance Minister : Dr. Yuvaraj Khatiwada

- Total Budget : NPR 1.315 trillion

Fiscal Year 2074/75

DOWNLOADBudget Speech For Fiscal Year 2074/75

- Budget At A Glance

- Prime Minister : Pushpa Kamal Dahal

- Finance Minister : Krishna Bahadur Mahara

- Total Budget : NPR 1,279 billion

Fiscal Year 2073/74

DOWNLOADBudget Speech For Fiscal Year 2073/74

- Budget At A Glance

- Prime Minister : KP Sharma Oli

- Finance Minister : Bishnu Prasad Paudel

- Total Budget : NPR 1.048 trillion

BUDGET IN NEPAL

The formulation of a budget is a decision-making procedure that sets out to produce a plan that forecasts revenues and allocates expenditures. A national budget in itself is a policy that governs the income and expenditure of a country. Besides, a national budget is also an indication of prioritized economic areas through inclusion of new projects and programs for development and economic growth on an annual basis. Budget is used as a tool that guides the efficient allocation of resources through expenditure accompanied by policies and planning decisions built into the budget. As a basis for determining the relationship between government programs, economic and financial policies and any shifts in government priorities, the budget of a country acts as a supporting framework for policies and laws.Budget is also a financial resource that plays a pivotal role in the functioning of the state. Whether a budget is balanced, in surplus or in deficit, directly influences the state's operation. A budget does not only establish a linkage with the existing policies but also addresses the demands of the citizens. The local level organizations, local representatives and parliamentarians have a vital role in advocating for certain programs or projects that meet the needs of their constituencies. Therefore, a budget represents an allocation of resources based on the demands and needs of the citizens.

The budget process is generally segregated into three phases: formulation, execution and evaluation. All these processes are interconnected and the attainment of a properly planned and executed budget is possible only if each phase follows the existing sets of guidelines and policies. It is evident that a country’s economy heavily relies on the effective formulation and implementation of a budget that is further dependent on adoption of the policies, timelines and laws developed for a systematic, transparent and appropriate execution of the budget.

Like most of the countries, Nepal is not new to the concept of budgeting, with detailed guidelines, policies, and laws in place. Though, the process of budget preparation to implementation is comprehensive, there have been numerous problems affecting it. Lawmakers and economists have argued that the existing framework of the national budget is not reflective of the true economic demands of the country. As budget implementation follows budget formulation, weaknesses and loopholes in the formulation process can transfer on to the latter phases. In the context of Nepal, the issue of significant proportion of the capital expenditure being unspent is indicative of the under- utilization of the resources in the country. Budget expenditure has always been a problem with majority of the spending taking place towards the end of a fiscal year. Such problems not only affect the economic functioning of the country but the functioning of the state too. Development is tied to the budget and problems in budget formulation and implementation have adverse effects on it. In Nepal, among the major problems surrounding budget formulation and implementation process, procedural delays, inter- agency coordination, local level participation, and management of funds are some of them. Each of these problems has contributed towards delaying the execution of the budget, leading to the underutilization of national budget every year.

The persistence of such problems in the budget making and implementing process forcibly delays the execution of national level programs and projects that are devised to attain certain development goals. Since budget is the document that releases national expenditure, these problems severely affect the spending levels of the state. Within the context, the absence to ascertain a mechanism that establishes a relationship between the central level authority and the local level authorities is also a challenge to the budget process. The policies and plans that have looked good on paper have failed to deliver the expected results. Hence it has been debated that the change in the existing framework is necessary to solve the existing problems related to the government's budget.

Only a sound understanding of the existing problems in budget process facilitates better planning and execution of state-level programs. Under this context, the paper reviews the existing budget formulation implementation procedures practiced in Nepal. While doing so, the paper focuses on capital budget, which a planning document usually targeting development. In course of the research, problems in capital budget formulation and implementation process related to transparency, management of funds, prioritization delay, procedural delays, and inter agency coordination have been the focus of the analysis.

Budget Formulation

1. Budget Forecasting

Forecasting is the first step in the budget making process where various macro-economic projections are made, sources of revenues and tentative areas of expenditure are identified and based on these economic targets are set. The Resource Committee of the NPC leads the forecasting process and produces fiscal aggregates. The committee is chaired by NPC's Vice Chairperson and includes other members of the NPC. The committee also includes members from the Nepal Rastra Bank (NRB), the MoF and the FCGO. The process commences when this committee reviews the revenue and expenditure for the ensuing fiscal year. The Economic Affairs and Policy Analysis Division of the MoF formulate the annual economic policy analysis and the macroeconomic forecast. The NRB also prepares forecasts based on growth estimates. Based on both projections, the Resource Committee decides on a macro-fiscal framework. Apart from this, the governmental plans of three years, five years and other macroeconomic goals set up by the NPC are also taken into consideration. The external and internal sources of revenue are also projected and referred to during this stage.Although these forecasts may not seem to have a direct linkage with the budget, they do affect the budget to a huge extent. The forecasting is the basis of the annual budget. Economic growth is targeted based on these estimates. Forecasting is a crucial step in budget formulation as its accuracy determines whether the budget will be balanced, in surplus or in deficit. We see the budget figures changing every year, and it is based on these forecasts that its gets altered. Forecasting is the first step that paves the path for other budget formulation activities. It is essential for the forecast to be comprehensive as it determines the nature and shape of the budget, and the indicators that define the forecast also define the economic objectives of the nation. Therefore any procedural issues affecting the forecasting phase are directly passed on to the subsequent phases.

2. Budget Ceiling Setting

Once a tentative forecast of the budget is prepared, it is presented to the budget committee comprising of members from the NPC and the MoF. The committee conducts extensive discussions regarding ceiling setting; an exercise that sets the limits on budget expenditure. A final shape to the budget is given at this stage. NPC also takes this opportunity to assess the budget utilisation and the progress of large-scale projects, which finally defines the scale of the capital budget. It is essential to set a ceiling on expenditures considering the limited resources. In the absence of such a ceiling, the request forwarded by the subordinate ministries may not be in line with the annual budget ceiling. This means that a considerable amount of time would have to be devoted to reconciling the ministry specific budget expenditures with the national level ceiling. Therefore, ceiling setting plays a vital role in limiting the size of the budget based on sectors and availability of resources.3. Budget Planning

After the determination of annual budget ceilings, the NPC requests the line ministries to submit their capital budget estimates in accordance to the guidelines and sectoral budget ceilings. Along with the NPC, the MoF issues detailed guidelines to the line ministries that require the budgets to be submitted in the prescribed format and within the stipulated time.At the local level, a meeting of the village council is called for discussing plans and programmes to be incorporated into the annual budget. Interest groups such as consumer committees, NGOs, political leaders and citizens are included in these discussions. Their plans are then forwarded to the VDC / municipality where it gets accumulated. Once the VDC scrutinizes and gives a green signal to the plan it moves up to the District Council which re-examines the budget and forwards it to the DDC. On the other hand, the district level development offices also forward their plans and budgets for the upcoming year to the DDC under the supervision of the relevant ministry. For instance, the health office in a district will make its plan according to the directives issued by the Ministry of Health and Population (MoHP) and forward it to the DDC and the concerned division or department of the ministry. The DDC then consolidates the budgetary demands of the health office with similar demands from different wards and sends it to the line ministry, which ultimately presents it to the NPC and the MoF for approval.

Once finalised, these plans are forwarded to the line ministry and then to the NPC. A tripartite discussion between the NPC, MoF and line ministry is held before finalizing the budget limits for the ensuing year. Upon receiving the budget requests, the NPC and the MoF compare various frameworks of the sectoral and national objectives. There is room for revision of the plans to achieve various programme targets for the upcoming fiscal year. The sectoral budgets are assessed in line with the budget ceilings. In the second round of the tripartite discussion, the MoF plays a crucial role where its main objective is to keep the budget within the approved budget ceilings. Meanwhile, the line ministries develop plans to achieve targets in diverse sectors which are reviewed by the NPC. Such projects are prioritised in the fiscal budget approved by MoF.

The budget formulation process displays both a bottom up and a top to bottom approach. This two way process is essential in creating a synergy between the national level plans and the local level needs. The actors in the central level authority are well versed with policies, plans, and guidelines while the local level actors are acquainted with the local needs, local capacity, and available resources in a particular area. It is when these two approaches coincide, that a fruitful expenditure plan of the budget can be obtained. This would ensure a budget that fulfils the demands of both the state and the locals.